Dividend Growers

Dividend Growers

Dividend Growers

Dividend Growers

Key Observations

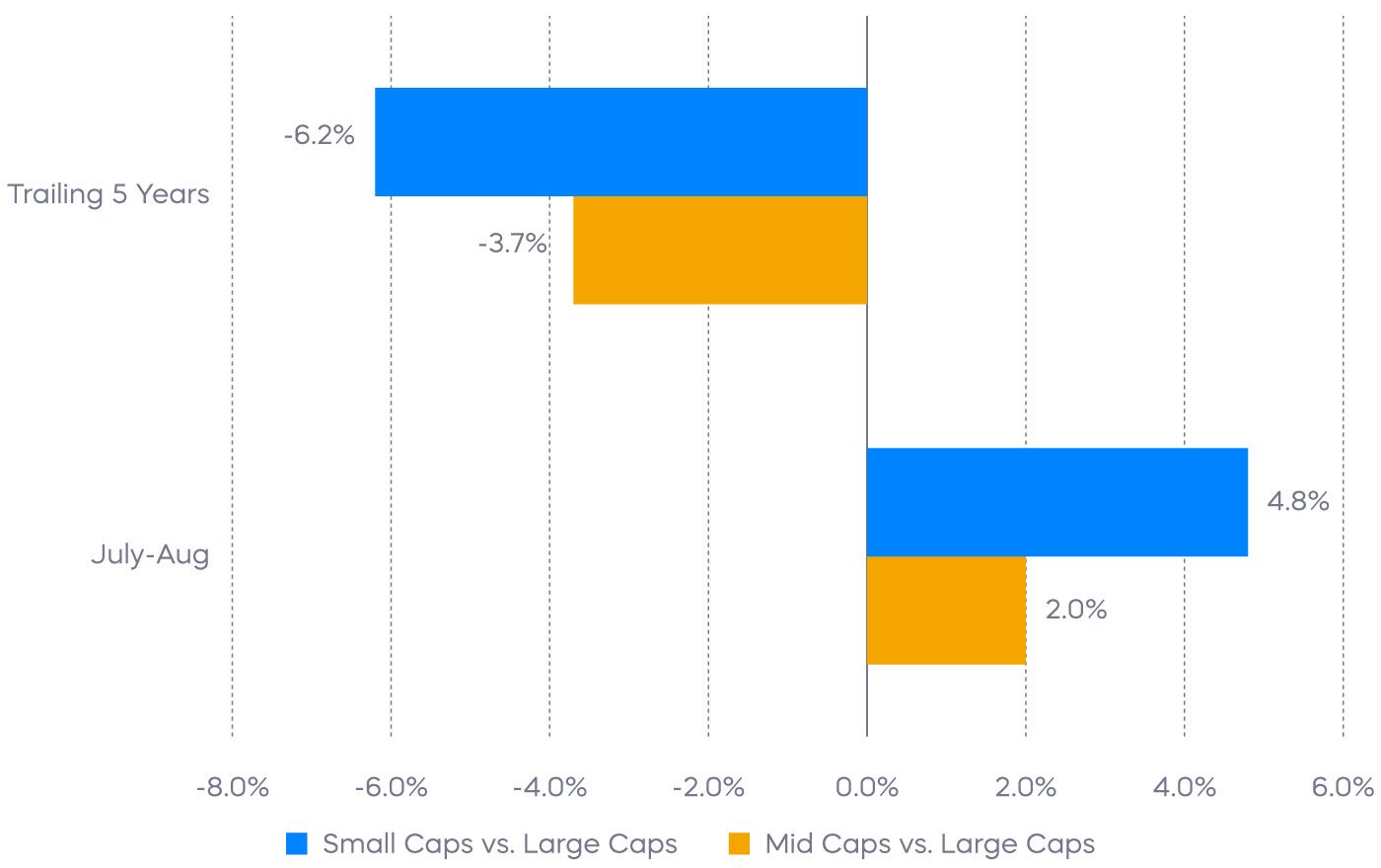

- After years of underperforming large-capitalization stocks, small- and mid-cap stocks (“SMIDs”) had a stellar mid-year, and with the Federal Reserve’s recent 50 basis point reduction in interest rates, they could be poised for a breakout.

- There’s still reason to be cautious, though, so investors may want to focus on quality stocks within the SMID segment for their potential to deliver all-weather performance.

- The S&P MidCap 400 Dividend Aristocrats and the Russell 2000 Dividend Growers could be well positioned in the current environment, trading at compelling valuations and with reliable earnings growth.

A Potential Breakout for Mid- and Small-Caps

Smaller-capitalization stocks unexpectedly raised investor eyebrows by delivering unusually strong performance in July. History has shown small-cap stock rallies can happen quickly, and July’s action was no exception. As is often the case, small-caps received most of the headlines, but mid-caps were also strong. Skepticism abounds as to the long-term sustainability of the rally, but after years of underperforming, conditions may finally be favorable for a breakout.

A Turning Point for Performance?

Source: Morningstar. Data as of August 30, 2024. Trailing five years performance is annualized. Large caps are represented by the S&P 500, mid-caps are represented by S&P MidCap 400, and small-cap stocks are represented by the Russell 2000 Index. Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

While some will point to tepid earnings growth or it being late in the economic cycle—typically not a favorable time for smaller stocks—other factors suggest that conditions could be right for a shift in market leadership away from mega-caps:

- Inflation has slowed and the Fed began cutting interest rates in September, which may be especially beneficial for smaller companies. They tend to borrow more than larger companies, so lowering their debt servicing costs could provide a catalyst for improved SMID stock earnings.

- Investors seem to have low expectations of SMIDs, reflected in what appears to be increasingly attractive valuations.

Today’s valuations are historically low—roughly 50% of large-caps on a price-to-book[1] basis. SMIDs haven’t been this cheap since the dot-com bubble burst at the turn of the century. Notably, smaller-cap stocks significantly outperformed large-caps for an extended period after that bubble burst (Source: Bloomberg, data as of 7/31/24). Considering this substantial valuation disconnect, further positive macroeconomic or fundamental developments could trigger a sustained rally.

Why Quality Matters for Small- and Mid-Cap Stocks

After an unusually tranquil period during the first half of 2024, market volatility returned with a bang in July. Much of the blame at the time was attributable to weakening economic indicators, potentially undercutting the soft-landing scenario. September’s 50 basis point rate cut came as welcome news, of course, driving equity markets to new highs. But uncertainty still remains, with the path likely to remain bumpy as we enter election season.

We believe the playbook in this scenario suggests leaning into high-quality dividend growth stocks like the Dividend Aristocrats, which have consistently grown their dividends over extended periods of time.

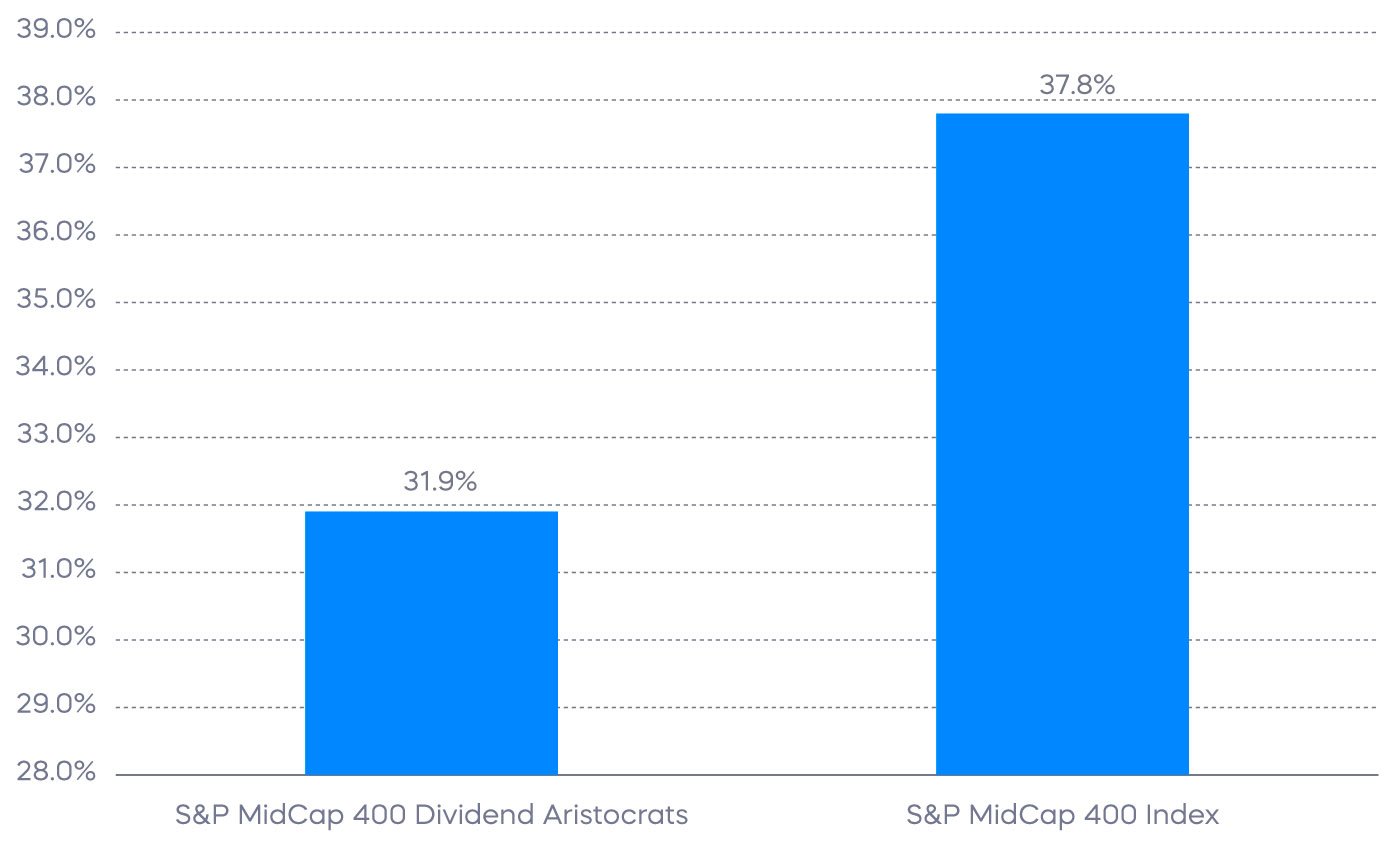

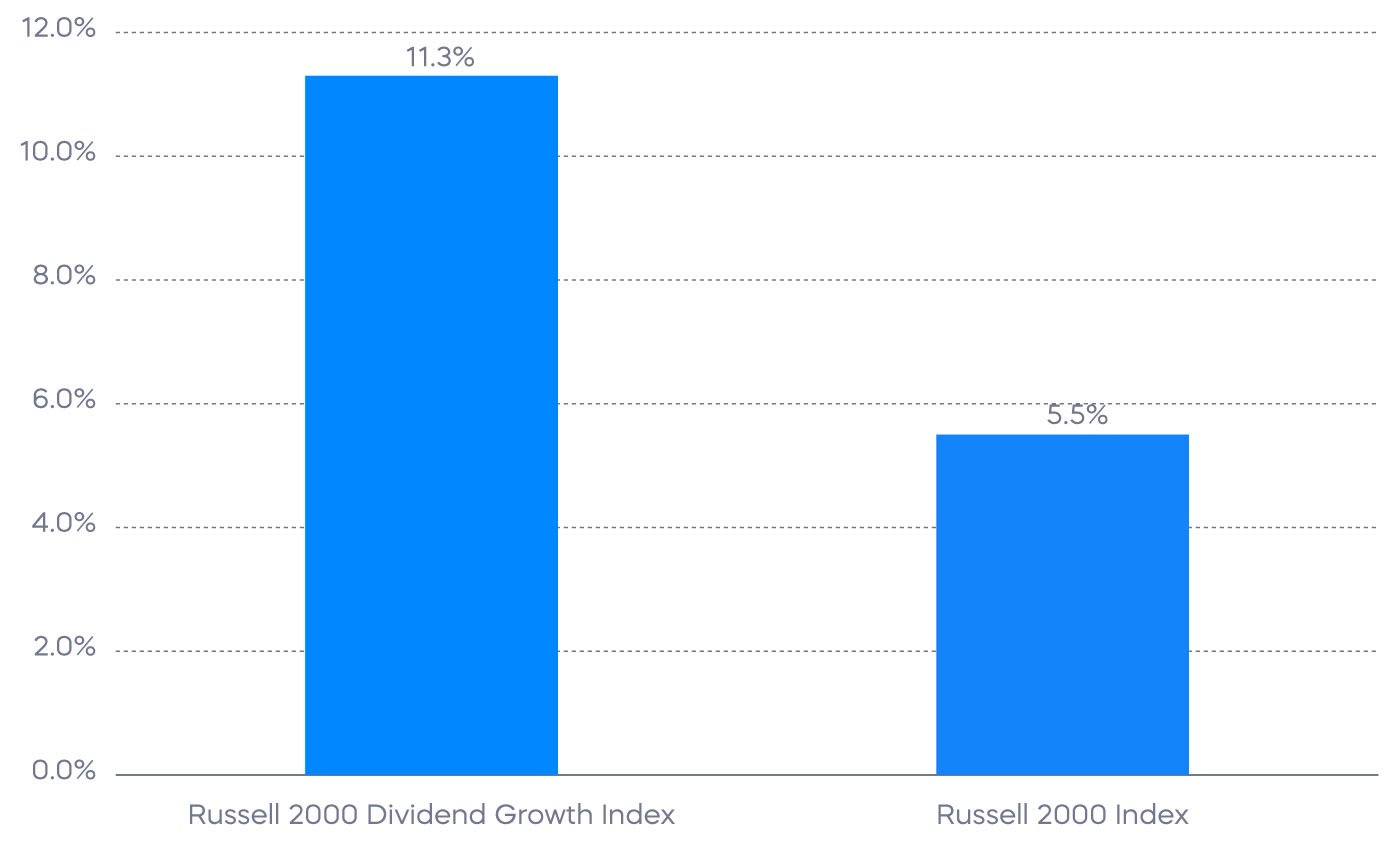

Quality typically degrades as one moves further down the cap spectrum, however, and unprofitable companies can be more plentiful. Small- and mid-cap dividend growers, on the other hand, have typically exhibited more financial flexibility, been less leveraged, and earned higher returns on equity than their broad market-cap peers.

Small-Cap Dividend Growers Have Had Greater Return on Equity

Source: FactSet. “Long-term debt to capital” is determined as of 7/31/24, calculated based on each individual index constituent’s long-term debt divided by its total capital, as reported by each constituent at its most recent fiscal reporting period. “Return on equity” is determined as of 7/31/24, calculated based on each individual index constituent’s net earnings divided by its shareholder equity, as reported by each constituent at its most recent fiscal reporting period. Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

The potential payoff in our quality-focused scenario comes back to fundamentals. Investing in dividend growers may remove some of the earnings uncertainty, and as we detailed in our August Market Commentary, both small- and mid-cap Dividend Aristocrats are expected to deliver positive earnings growth for the remainder of 2024.

Dividend Aristocrats Have Delivered All-Weather Performance

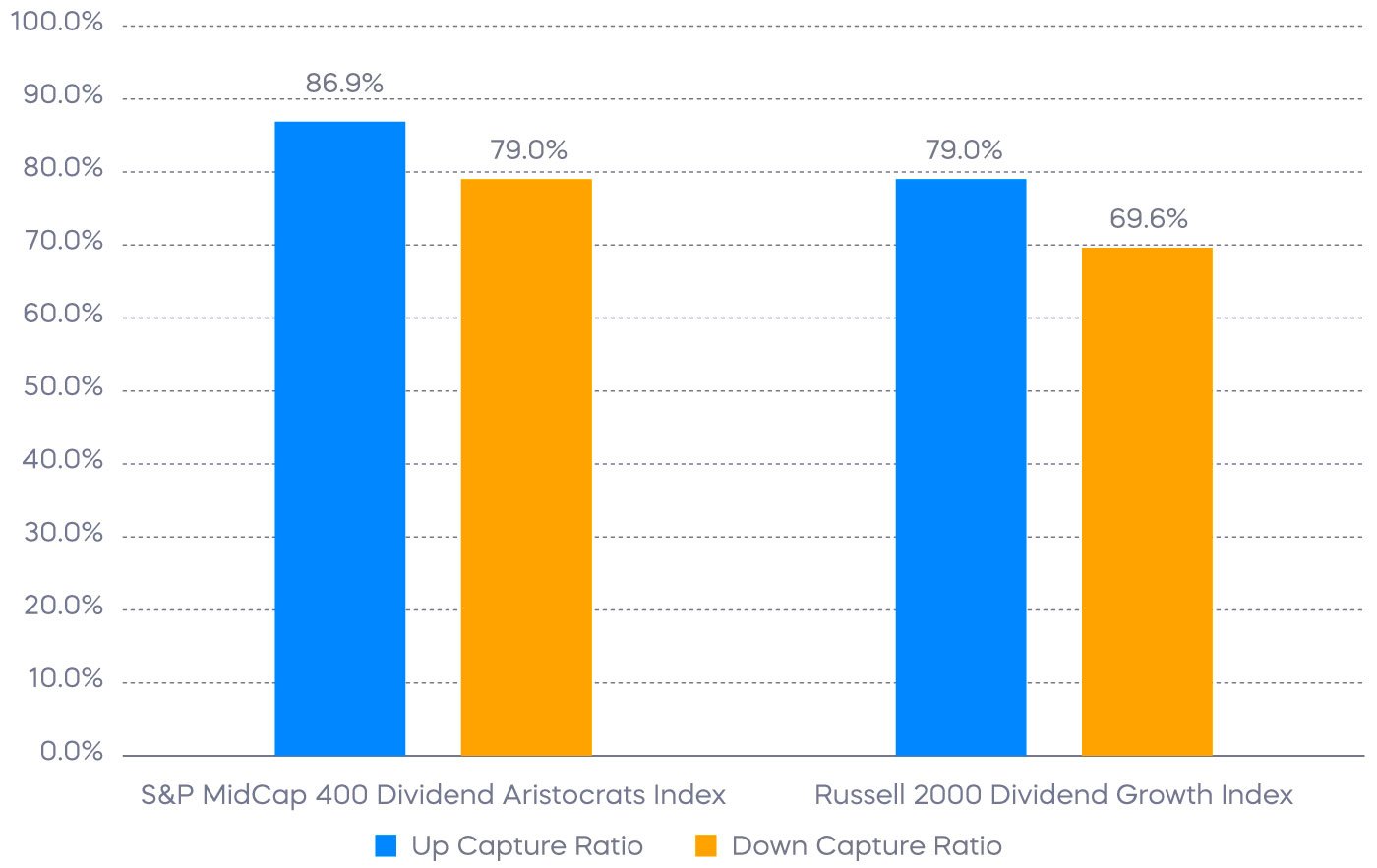

The generally higher-quality profile of its dividend growth stocks has helped both the S&P MidCap 400 Dividend Aristocrats Index and the Russell 2000 Dividend Growth Index to outperform their broad benchmark indexes since inception, and to do so with less volatility.[2] They have also delivered all-weather performance, regardless of the economic environment.

Small- and Mid-Cap Dividend Growers Have Delivered All-Weather Performance

Source: Morningstar. S&P MidCap 400 Dividend Aristocrats Index data from 2/1/15–7/31/24, and Russell 2000 Dividend Growth Index data from 12/1/14–7/31/24. Index returns are for illustrative purposes only and do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

- For investors seeking some all-weather stability, the S&P MidCap 400 Dividend Aristocrats have historically delivered 87% of the S&P MidCap 400’s upside performance, with only 79% of the downside.

- The Russell 2000 Dividend Growers have delivered 79% of the upside performance and only 70% of the downside compared with the Russell 2000 Index.

The Takeaway

After years of them underperforming large-caps, are we finally witnessing a rotation to small- and mid-cap stocks? Having significantly outperformed in July, and with the added boost of September’s interest rate cut, small- and mid-cap stocks could be due for a breakout. But with election and other uncertainties still looming, investors may wish to consider a focus on higher quality SMID strategies like the Dividend Aristocrats and their potential to deliver all-weather performance.

[1] Price-to-book compares a firm's market capitalization to its book value, and it is typically used by investors to help identify companies that may be undervalued.

[2] Source: Bloomberg. S&P MidCap 400 Dividend Aristocrats Index performance is from 1/5/15 (index inception) to 7/31/24. Russell 2000 Dividend Growth Index performance is from 11/11/14 (index inception) to 7/31/24.

Learn More

NOBL

S&P 500 Dividend Aristocrats ETF

Seeks investment results, before fees and expenses, that track the performance of the S&P 500® Dividend Aristocrats® Index.

REGL

S&P MidCap 400 Dividend Aristocrats ETF

Seeks investment results, before fees and expenses, that track the performance of the S&P MidCap 400® Dividend Aristocrats® Index.

SMDV

Russell 2000 Dividend Growers ETF

Seeks investment results, before fees and expenses, that track the performance of the Russell 2000® Dividend Growth Index.

Dividend Growers

Dividend Growers